Framework for Understanding ACA Market Structure and Risk Adjustment Programs Series

ACA Marketplace Primer - Part 1

This article outlines the fundamental structure of the ACA marketplace, its participants, and various coverage programs. Understanding these basic components creates a foundation for exploring more complex aspects of ACA, particularly the Risk Adjustment Program which manages the distribution of financial risk among insurers based on their enrolled populations' health status.

Affordable Care Act

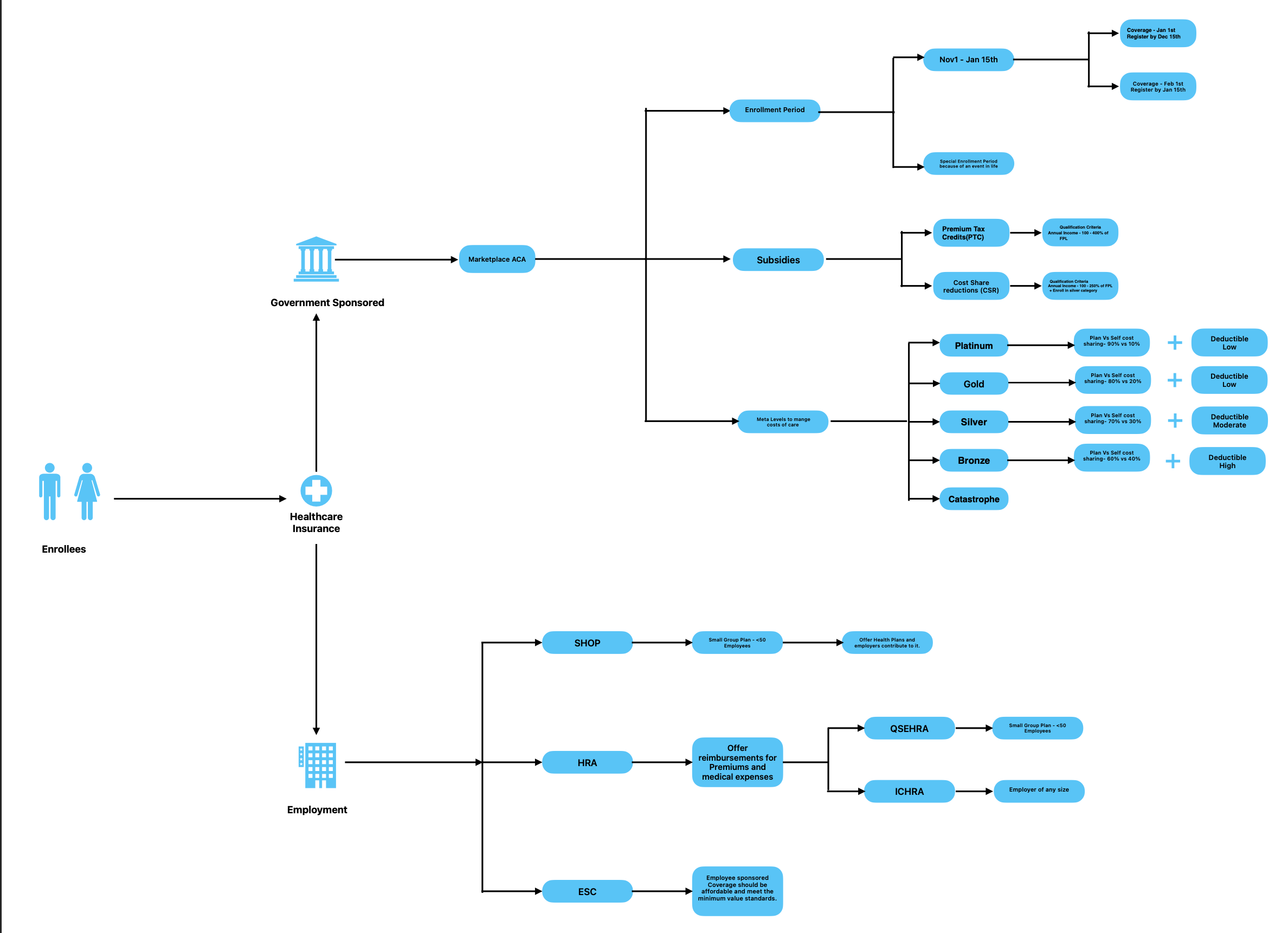

The Health Insurance Marketplace, created under the Affordable Care Act (ACA), offers a straightforward way to compare and purchase health insurance. Think of it as a shopping center for healthcare plans, where every plan must meet certain quality standards.

When Can general public Enroll?

Annual Open Enrollment : November 1 - January 15

Want coverage by January 1? Sign up by December 15

Enrolling between December 16 - January 15? Your coverage starts February 1

Life changes like marriage, moving, or job loss? You might qualify for a Special Enrollment Period

Understanding Metal Tiers: How Much Will members Pay?

Insurance plans come in different metal tiers, each representing how you and your insurance company share costs:

Platinum: Insurance covers 90%, you pay 10% - Best for frequent healthcare needs

Gold: Insurance covers 80%, you pay 20% - Good for moderate healthcare needs

Silver: Insurance covers 70%, you pay 30% - Popular middle-ground option

Bronze: Insurance covers 60%, you pay 40% - Lowest monthly premiums

Catastrophic: Basic coverage for healthy people under 30

Note: Lower monthly premiums usually mean higher out-of-pocket costs when you need care.

Financial Assitance

The ACA provides two main types of financial assistance:

1. Premium Tax Credits (PTC)

- Help reduce your monthly insurance bill

- Available if your income is between 100-400% of Federal Poverty Level

- Applied directly to your premium or claimed on tax returns

2. Cost-Sharing Reductions (CSR)

- Lower your out-of-pocket costs like deductibles and copays

- Available if your income is between 100-250% of Federal Poverty Level

- Must enroll in a Silver plan to qualify

Employment-Based Options

1. Small Business Options (SHOP)

For businesses with fewer than 50 employees:

- Employers can offer group health plans

- May qualify for tax credits

- Employees get group coverage rates

2. Health Reimbursement Arrangements (HRA)

Two modern options for employers:

QSEHRA (Small Businesses)

- For employers with fewer than 50 employees

- Tax-free reimbursement for medical expenses and premiums

- Annual contribution limits apply

ICHRA (Any Size)

- Available to employers of any size

- Flexible design options

- Can offer different amounts to different employee classes

3. ESC (Employee Sponsored Coverage)

Employer-provided health insurance must be affordable

Must meet minimum value standards

Plan must cover at least 60% of total allowed costs

Must provide substantial coverage of physician and inpatient hospital services

There is always more to learn and share. Please share your feedback and if there are additional topics that might be of value.

Sources:

https://www.healthcare.gov/

https://www.cms.gov/marketplace/eligibility-enrollment-resources/coverage-effectuation-webinar

https://www.cms.gov/marketplace/technical-assistance-resources/aptc-csr-basics.pdf

https://www.cms.gov/marketplace/technical-assistance-resources/aptc-csr-basics.pdf